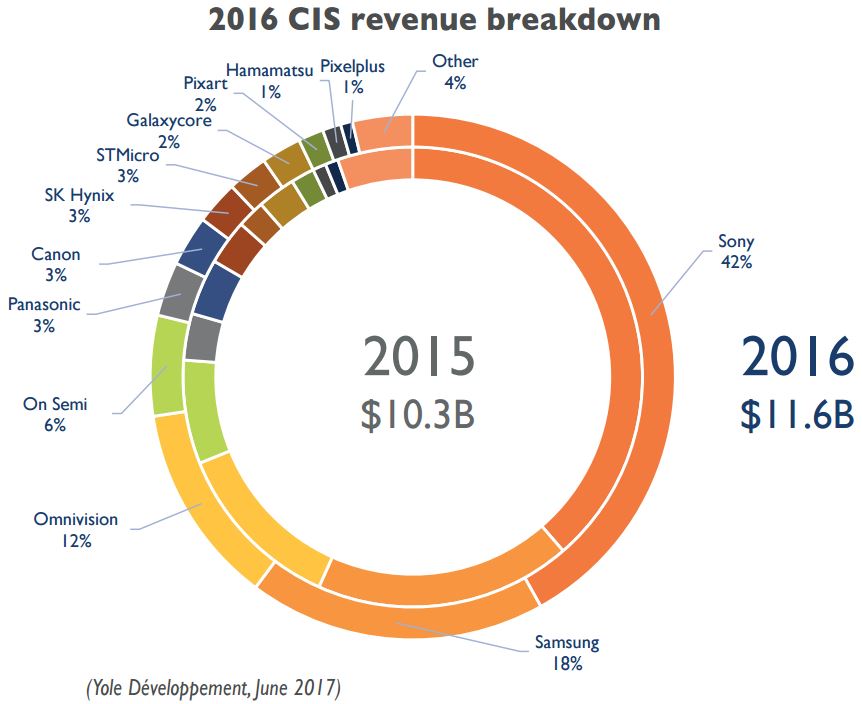

"CMOS imaging has benefited from huge market demand and a technology-driven environment, resulting in an $11.6B industry in 2016.

The mobile market is key for the CMOS image sensor (CIS) industry. Despite saturation in the number of handsets, the CIS market has been able to maintain a 10.5% compound annual growth rate (CAGR) for the 2016-2022 period due to the introduction of dual and 3D cameras.

Sony has established itself as industry leader, market and technology wise. However, the 2016 earthquake in Japan slowed down its operation and helped maintain the growth of its close competitors. Indeed, despite Toshiba’s exit from the market, two thirds of players have seen growth in the last year. Samsung, Omnivision and Panasonic have delivered 15% year-on-year growth. Those large players are increasing the weight Asia carries in the CIS industry.

In the US, On Semi has suffered from the public relations mess that followed a fatal crash involving Tesla’s semi-autonomous driving system, which included a Mobileye sensor. Automotive cameras are safety-critical and therefore the reaction is strong if performance does not match expectations.

Another noticeable activity has been STMicroelectronics’ revival of its CIS business through the development of 3D ‘Time of Flight’ (ToF) devices. They will probably be the biggest event of the end of 2017, if they materialize in the Apple iPhone 8 as is rumored.

The impact of 3D semiconductors is currently a key element of the competition. Samsung has finally joined Sony as a provider of stacked back-side illuminated (BSI) sensors. Omnivision and SK Hynix will also soon launch this technology. Meanwhile, SMIC and STMicroelectronics will probably be the next players to unveil their versions of stacked technology.

Increases in CIS production capacity have momentarily stopped due to this stacked trend. This is currently mainly due to Sony, which can source its logic wafers from TSMC. In coming years Sony, Samsung, STMicroelectronics, HLMC and SK Hynix will all announce extra CIS capacity in order to meet market demand, despite stacked BSI adoption."

No comments:

Post a Comment

All comments are moderated to avoid spam and personal attacks.